On this page

Most funded accounts are simulated. The live program sits behind them as a gated tier almost no trader reaches, and the move itself takes back profit you already earned. Here is how these programs work, in the firms’ own published rules, and where we stand on them.

A prop firm live program is the stage where you stop trading a simulated account and start trading the firm’s actual capital in the real market. Most traders assume that happens the moment they pass an evaluation. At nearly every major prop firm, it doesn’t. The account you get after passing is a demo account that pays real money on simulated results, and the live program sits behind it as a separate, gated tier that the firm decides when you enter.

This article takes a side, so here it is up front. We run Breakout, and we believe the majority of live programs function as one more mechanism that trips up profitable traders and reduces what firms end up paying of the profit those traders already earned. Firms describe these programs as graduation, or as prudent risk management. Their published transition terms, which we walk through below, read differently: accounts closed, profit above a cap forfeited, a new rulebook, lockouts measured in weeks. Breakout runs no live program at all: one rulebook from evaluation through payout, a drawdown floor set on day one that never moves, and withdrawals on demand. The full contrast is at the end.

The industry mechanics come first, because you shouldn’t take our word for any of this. The figures below come from firms’ own published help pages and program documents, verified in July 2026. Prop firms change rules often, so treat any specific number as a snapshot, and check the live pages yourself.

The Three Stages Behind the Word “Funded”

The standard structure across the industry, and especially at futures prop firms, is a three-stage funnel.

Stage one is the evaluation. You pay a fee and trade a simulated account against a profit target and drawdown limits. This part everyone knows.

Stage two is the simulated funded account. You passed, and the firm now calls you a funded trader. The payouts are real. The capital is not. You are trading a demo account, and the firm pays you a share of the simulated profit. This is where the overwhelming majority of funded traders spend their entire time with a firm.

Stage three is the live account: the firm’s actual capital, deployed in the real market. Entry is not automatic and not something you apply for. The firm’s risk team decides who moves, and when.

How few traders reach stage three is not a matter of speculation. One of the largest futures prop firms publishes its own program statistics, and its 2025 figure was 0.71%: that share of its simulated funded traders were called up to a live account. The other 99.29% stayed in the simulation.

How a Prop Firm Live Program Transition Works

If the live tier were simply a promotion, none of this would matter much. It’s the terms of the transition that deserve attention, and they follow a consistent shape across firms.

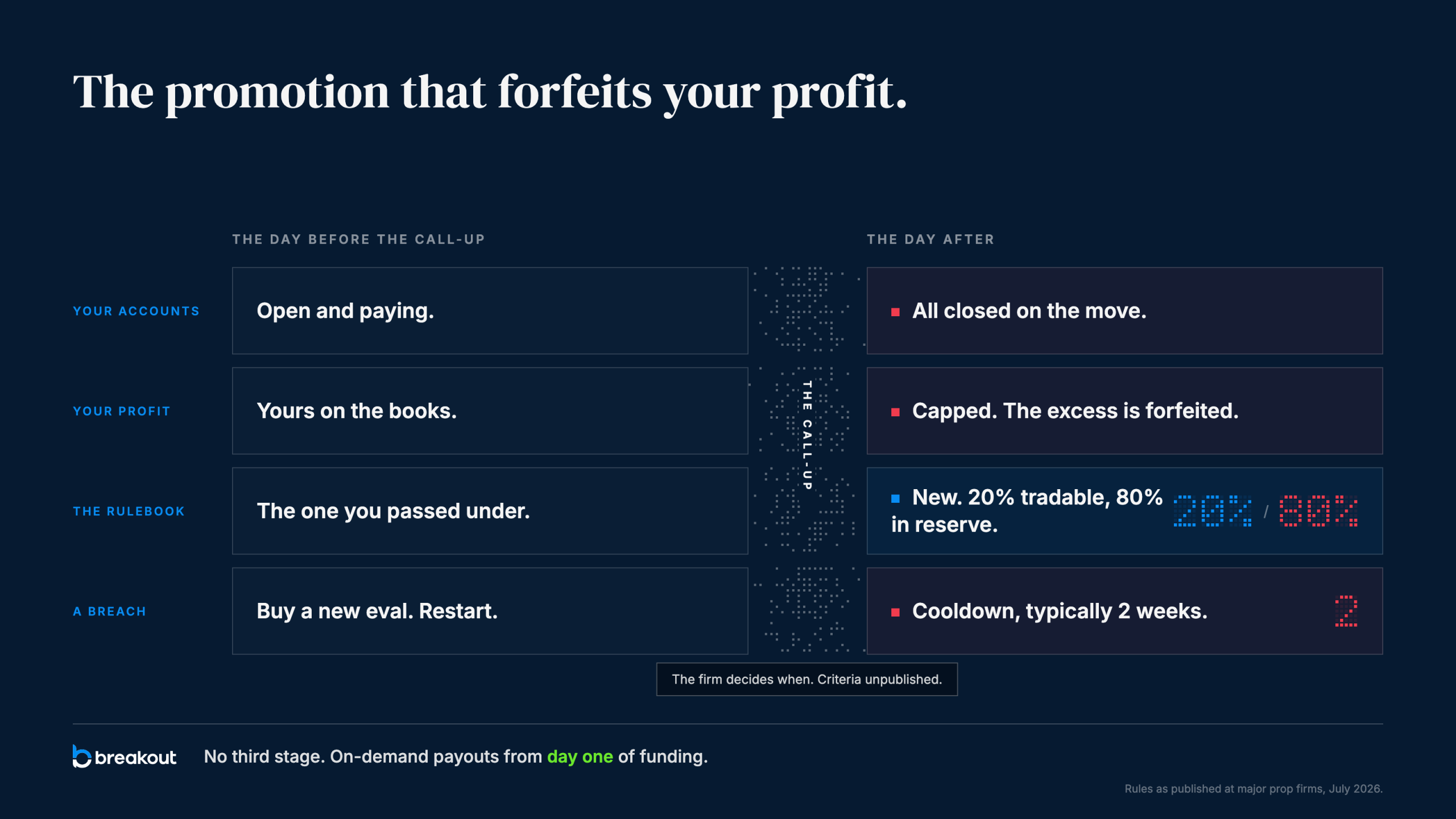

The trigger is discretionary. Firms state that the risk team moves traders based on demonstrated consistency, at a time of the firm’s choosing. Some publish partial criteria. One crypto-adjacent firm currently generating industry discussion says a trader enters its live review pool after a fifth payout, after significant lifetime payouts, or whenever its risk team decides. The precise threshold is unpublished at almost every firm. You cannot plan for it, and at major firms you cannot decline it either: one states that rejecting the move is not possible once you are selected, and another gives you two options, move to live or close your accounts.

Your simulated accounts close. When the call-up happens, the accounts you were being paid from get shut. Every firm that documents the transition states this. If you were running five accounts, the transition ends all five.

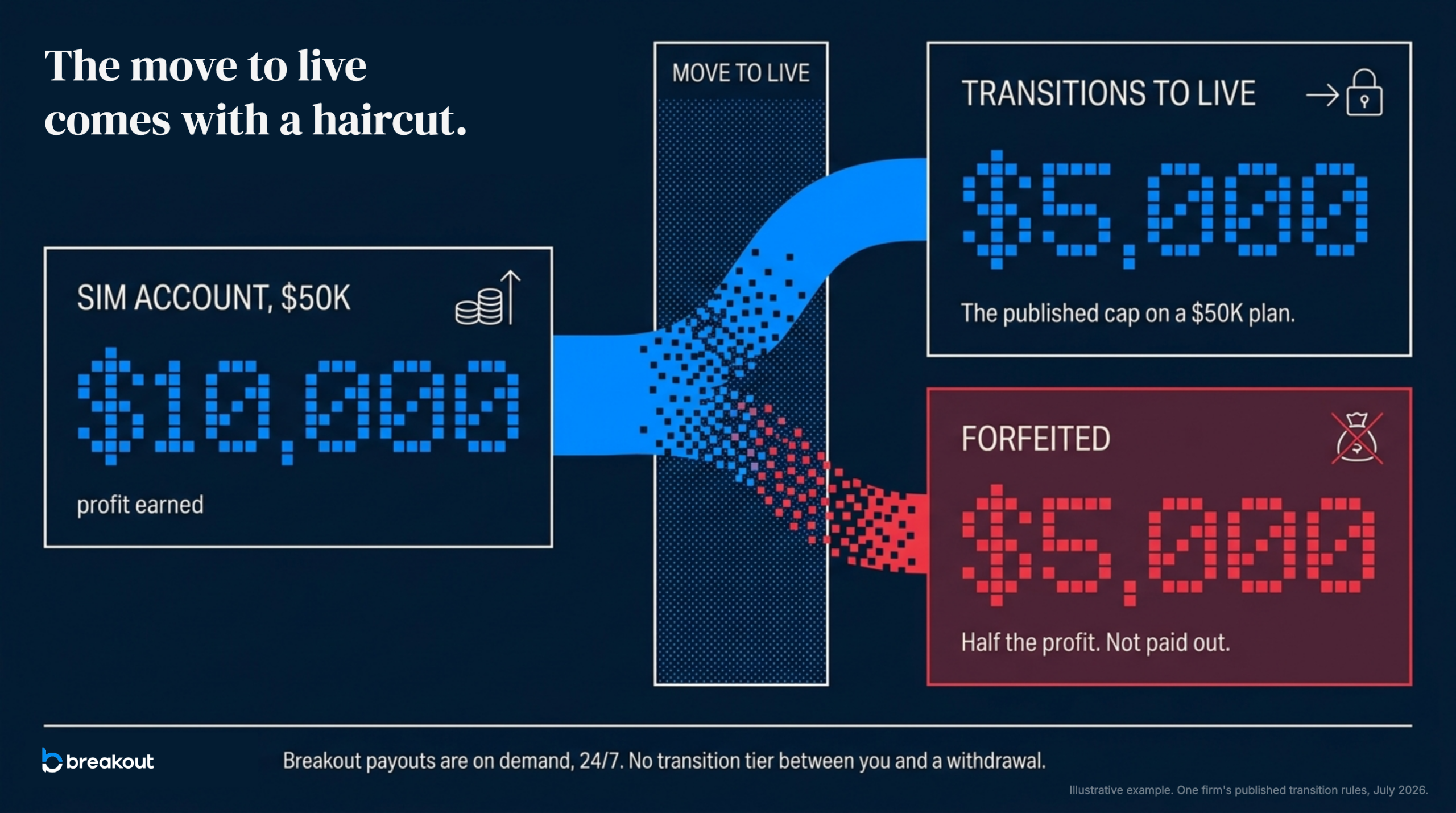

Profit above a cap is forfeited. This is the sharpest edge, and it’s stated plainly in the firms’ own documentation. One firm’s help center says that on transition to live, profits move across up to a per-plan cap and, in its own words, “remaining profits are forfeited.” Its published cap on a $50,000 account is $5,000. Make $10,000 in sim profit on that account and the promotion costs you half of it. Another firm ran a cap-and-escrow version of the same structure until early 2026: its published worked example had a trader moving five $50,000 accounts forfeit $2,000 per account, with what survived the cap held in escrow against live performance benchmarks. That firm’s current structure removed the cap by removing the transfer entirely. Live accounts now start at a $0 balance, and the simulated profit stays behind.

The rulebook changes. Live accounts run different parameters than the simulated accounts that earned the promotion. One major firm’s live accounts start with 20% of the balance tradable while the other 80% sits in a reserve that unlocks at profit milestones. You proved yourself under one set of rules and now trade under another.

A breach means weeks of lockout. Blow the live account and you don’t buy a reset the next morning. The published standard at one firm is a two-week cooldown, longer if the firm judges the trading reckless.

There are adjacent mechanics worth knowing even before any live transition. One large futures firm closes each simulated funded account after its sixth payout, requiring the trader to buy a new evaluation to continue. Another freezes $5,000 of accumulated profit as collateral for as long as its live-tier account stays active.

Put the pieces together and the pattern is clear. The live program activates precisely when a trader has proven consistently profitable, and every published transition mechanic reduces what that trader collects: closed accounts, capped and forfeited profit, escrowed balances, a tighter rulebook. Firms present this as graduation. Our read is less generous: we think most of these programs operate as one more tripwire between a profitable trader and the money they earned. Judge for yourself, but judge from the documents, because everything above comes from the firms’ own pages.

The Buffer: Profit You Earned but Can’t Withdraw

The second mechanic sits inside the simulated funded stage itself, and it governs the relationship between your payouts and your drawdown.

At almost every firm, a slice of your account equal to your maximum drawdown stays locked and cannot be withdrawn. Firms call it a buffer, a safety net, or a reserve. One firm’s published version: on a $50,000 account with a $2,000 drawdown limit, your balance must reach $52,000 before any withdrawal is possible, and only profit above $52,000 is withdrawable. Another sets its safety net at the drawdown limit plus $100, in place for the life of the account.

The buffer is not returned when you’re done, or not fully. The firm with the $52,000 threshold releases the buffer only when the account closes, and only in part: 50% of it if the account traded 60 trading days or fewer, 80% if longer. The rest is kept.

So the first $2,000 you earn on that account is money you can see, cannot touch, and may never fully receive. It exists so the account survives your own withdrawals, which brings us to the mechanic that actually defines these programs.

The Floor That Only Moves Up

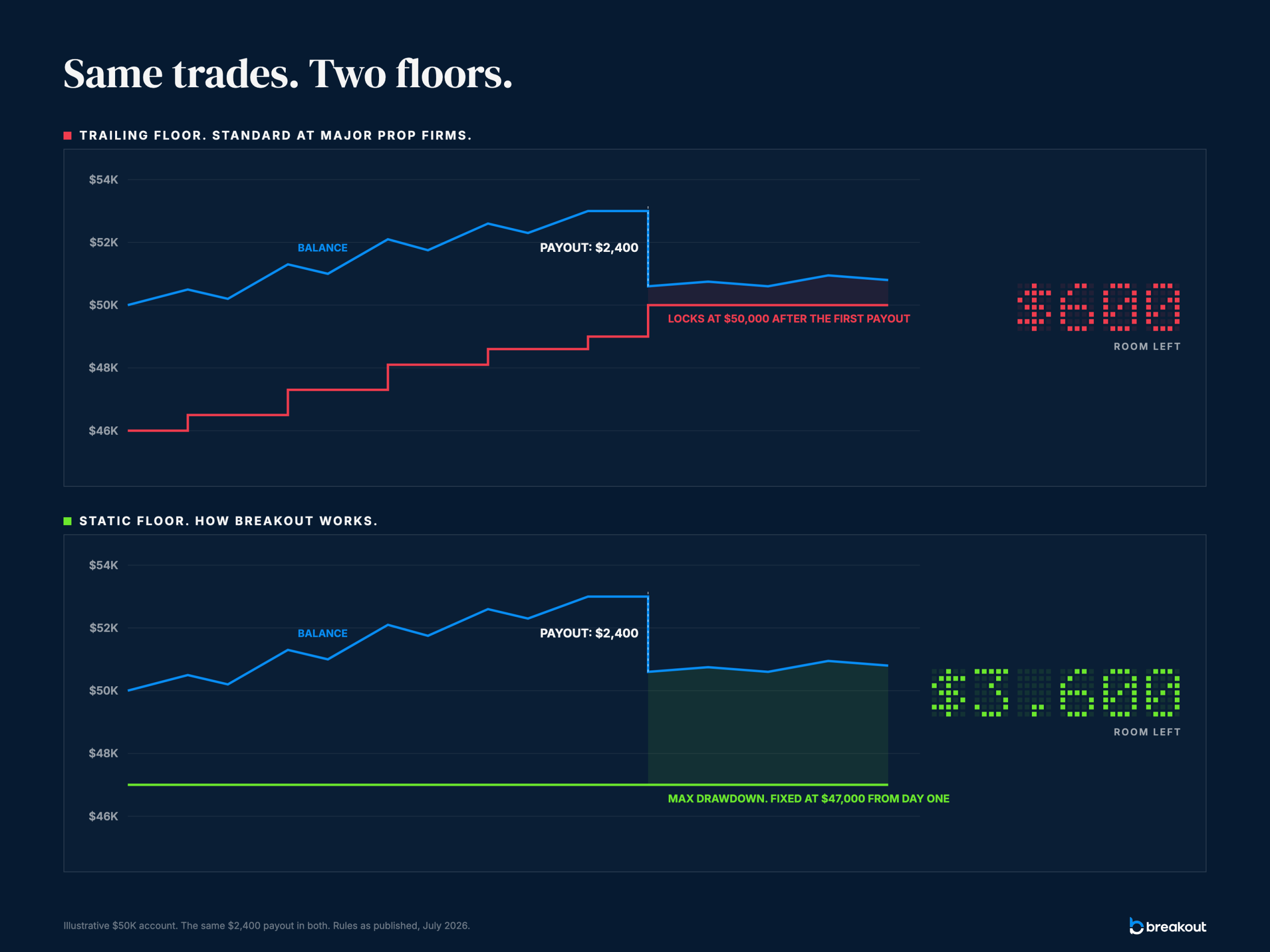

At most firms, your drawdown floor is not fixed. It trails your balance upward as you profit. It does not come back down when you withdraw.

Walk through what that means. You grow the account, and the floor climbs behind you. You request a payout, and your balance drops by the amount withdrawn. The floor stays where it was. You are now sitting closer to a breach than you were the moment before you got paid.

The firms say this themselves, in their own instructions to traders. One of the largest futures firms tells traders to trade as if the requested payout amount has already been removed from the balance. Another deducts the payout from the balance immediately, and after the first payout sets the maximum loss limit to $0, breakeven on the starting balance, permanently. From that point, there is no cushion below the starting balance, and every subsequent payout pulls the balance back down onto a floor that no longer moves at all.

Multi-asset firms run their own versions. One publishes a per-cycle payout cap with a worked example: on a $100,000 account, make $7,000 and you can request the $5,000 cap, while the remaining $2,000 stays locked in the account as drawdown you can never request. The same firm sets its drawdown level up to the starting balance at the first payout, permanently: the floor rises to breakeven, and the only room left above it is whatever profit stayed locked in the account.

The one-line summary of all of this: at most firms, taking a payout increases your breach risk. The act the whole arrangement is supposedly built around, getting paid, is the act that moves you closest to losing the account. If a firm wanted a mechanic that quietly discourages withdrawals, it would look exactly like this one.

Five Things to Check Before You Pay for an Evaluation

None of these mechanics are secret. They sit in help centers and FAQs, and reading them before you pay is the whole game. Specifically:

- Is the funded account simulated, and is there a separate live tier behind it? If the answer is yes, find the transition terms.

- What happens to your accounts and your open profit if the firm moves you to live? Look for the words “cap,” “forfeited,” and “escrow.”

- Does the drawdown floor trail your balance, and does it come back down after a withdrawal? If it trails and locks, every payout raises your risk.

- How much of your profit sits in a locked buffer, and under what conditions is it ever released?

- Are the promotion criteria published, and does the firm publish how many traders reach live? One firm’s own number is 0.71%. Ask why others don’t publish theirs.

If a firm’s documentation answers these clearly, you can make an informed decision. If it doesn’t, that is also an answer.

How Breakout Handles the Same Mechanics

Breakout runs no live program, and that’s a position, not a gap in the product line. Breakout is a crypto prop firm backed by Kraken, and the contrast is easiest to see mechanic by mechanic, because the answer to most of the questions above is that the mechanic doesn’t exist here.

There is one rulebook. The account you pass into runs the same two loss limits as the evaluation you passed: same max daily loss, same max drawdown. There is no separate program behind the funded account, no discretionary call-up that closes your accounts, and no transition that caps or forfeits profit you already earned.

The floor never moves. Breakout uses static max drawdown, set once at account creation from the starting balance. On a $100,000 1-Step Classic account with 6% max drawdown, the floor is $94,000 on day one and $94,000 forever. Make $8,000, withdraw $8,000, and your balance returns to $100,000 with the full $6,000 cushion still under it. A payout does not move you toward a breach, because the floor was never derived from your peak balance in the first place.

Worth addressing before someone raises it: Breakout’s second limit, max daily loss, does recalculate every day, at 3% of your balance at the daily reset. That’s a pacing limit, not the account floor, and it behaves nothing like the ratchet described above. It tracks your balance in both directions, down as well as up, so a payout never strands it above you; the next reset derives it from whatever your balance is now. And the reset closes nothing. Crypto has no end of day, positions hold straight through it, and swing trading works fine.

Payouts are on-demand, 24/7. No payout cycles, no per-cycle caps, no minimum trading days, no account closure after a set number of withdrawals. The minimum is $50 after the profit split, paid in USDC. You keep 80% of profits, with 90% available as an upgrade. Breakout has paid $50M+ to traders since launch, and the payout leaderboard is public if you want to check rather than take the claim on trust.

To be direct about what this is and isn’t: trading is still risk, the evaluation fee is still at risk, and Breakout profits from evaluation fees. The difference described here is structural, and you can verify every parameter in the published rules before paying anything. That’s the standard worth holding any firm to, including this one.

A live program is the stage most funded traders never see, at firms where getting paid moves you closer to losing the account. We think that arrangement fails the traders it claims to reward, and we built Breakout without one. Read the transition terms and the drawdown mechanics before you pay, at any firm, including ours.

Competitor mechanics referenced above are drawn from the relevant firms’ own published help centers and program pages, verified July 2026. Rules change frequently; always confirm against the live documentation.